April 30, 2020

The study of market bubbles is now pretty commonplace and so this doesn’t add anything to that study, but it does highlight some interesting ideas about the markets we are in, in case you need more reasons to protect your assets.

First off, what is a bubble? Prices for many assets move above and below their true value all the time. This is easily seen in the price movement for assets traded regularly, such as a company stock. A bubble however is different in that it represents a significant divergence between an assets price and its true, underlying value. Famous bubbles have happened all through history.

Knowing that this divergence between price and value happens leads to all sorts of potential arguments about how to price things and how to measure their underlying value.

While I would like to delve into this with many assets, this post comes to me after reading a column in the real estate section of Toronto’s Globe and Mail this morning, so I will focus on real estate primarily.

Here are two quotes from that column that raised my eyebrows:

“for the past decade or more of rising values, it has been hard to imagine a Toronto-area condo presale unit selling late in a cycle for less than the early access sales price” and later, “We gathered 2000 brokers and there was only 593 units in the building”.

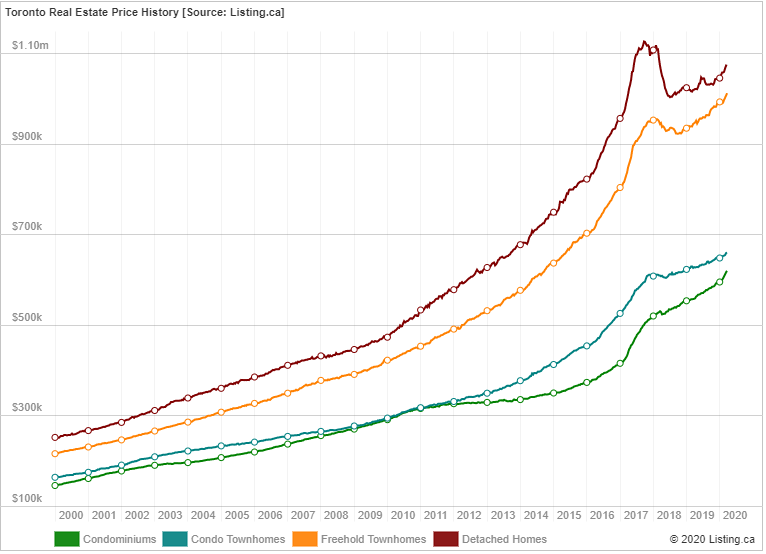

In the case of a home, an accurate assessment of price can only reasonably be determined when the home sells between buyers and sellers working at arms length. To understand what a fair price is, one typically uses sales of similar homes and then guesses at the fair price. Here is the price history for homes in the Greater Toronto Area (GTA) from ‘toronto.listing.ca‘.

If you bought any home at any time, except perhaps 2017 you would be quite pleased with the price of your home or investment. Of course it could take a long time to understand if your price truly reflects the underlying value. How do your determine value?

There are a number of ways to determine value. You can look at the replacement value of a home; that is how much it would cost to build a similar home on a similar lot (or buy one in a similar building in the case of a condominium).

You can look at the economic value of a home. If your home is the place you live, then this relates to your earnings and disposable income after all of your other obligations are met. If it is for investment, then its the income left after all the rental income and costs are tallied, with allowances for things like vacancies and maintenance.

In a world where people are competing, sometimes very aggressively, for almost anything, prices get out of step with value. Ultimately that is how bubbles manifest themselves.

So are we in a bubble? In a word, yes. But that’s not the whole story, so read on.

The Huffington Post published a nice article in January of 2019 highlighting the wackiness of Canada’s real estate market, and it shows a nice chart (sourced from the Economist) of house prices relative to income.

This chart makes it clear that we can no longer afford the places that we live. The real estate broker mentioned in the article above marvels at how no one has lost money by buying a pre-sale condo and then selling it later. Even further, bragging how they would have significantly more brokers (who may represent dozens of clients) at a sales event for a modest number of condos.

One answer is that this is a supply and demand problem. That is the same argument used in the UK when Russians came in and started buying up all of the high end properties, pushing prices higher. It is the same argument used in Vancouver when offshore buyers came in and bought up large swaths of condominiums. It is the same argument around the world when landlords purchase swaths of real estate for short term rentals such as AirBNB and VRBO.

The low supply narrative fits well with the quest for land by developers and excellent cover for the rising prices for rent as well. It fits well for cities that want to increase their tax base, for banks that want to lend more money and for real estate agents who want to make more commissions.

The whole deal is a major engine in the economy! Currently real estate, including rental and leasing represents more than 14% of Canada’s GDP. In the US, it represents 6.2% of GDP. That excludes the construction and banking components.

So are we in a bubble? Again, yes.

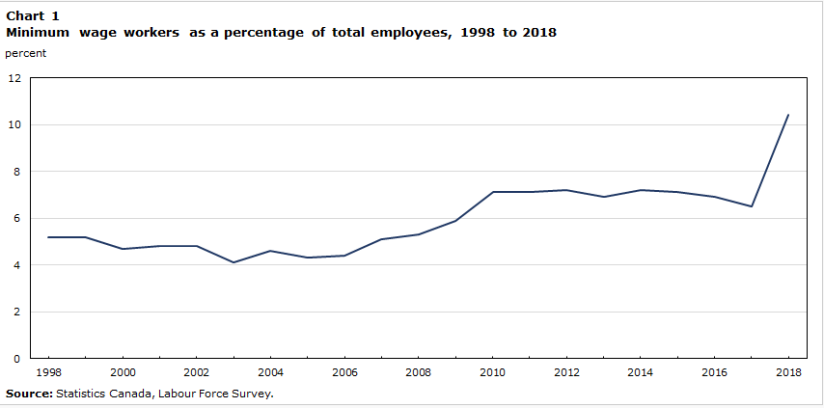

The income required to sustain the prices (even if there is insufficient supply) will not be forthcoming. In the first chart below, we see the number of minimum wage workers as a percentage of total employees in Canada. The rise since 2008 is significant and the current crisis is going to make it worse.

The second chart shows non-union wages in Canada. Union wages are slightly higher, but the noteworthy component is that average wages have grown 69% over the past 20 years while home prices have grown by over 400%.

The second chart shows non-union wages in Canada. Union wages are slightly higher, but the noteworthy component is that average wages have grown 69% over the past 20 years while home prices have grown by over 400%.

How is this possible? There is really just one answer. Interest rates. The prime mortgage rate in Canada has declined from 14.75% in 1990, to 7.5% in the summer of 2000 and for the past 10 years has spent much of the time between 2.7% and 3%. In mortgage terms, that means that a $1,678 payment would get a $300,000 home in 2000, but now a buyer can afford about $520,000 with the same payment.

The bubble part comes in when considering that the value of a home hasn’t changed much. Homes of all types are smaller, with less space inside and out. Density is rising sharply in urban areas.

It remains to be seen if this bubble bursts (they all do, sooner or later) and more importantly if COVID-19 will bring on the change, but for those that are interested in a longer term perspective, here is a history of home values by Yale Economist Robert Shiller up until 2010. Shiller’s name adorns the Case/Shiller home price index in the US, one of the most widely followed housing statistics and it reminds us that prices for real estate, like stocks, do decline.

The above is an excellent long term view, and below is the chart from a current source with the data from 2000 to February 2020, just before the COVID-19 outbreak was recognized as a threat to human life in North America.